Saturday 15 November 2025

Latest

E-Paper

বাংলা

Previous Month

November 2025

January

February

March

April

May

June

July

August

September

October

November

December

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Su

Mo

Tu

We

Th

Fr

Sa

26

27

28

29

30

31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

1

2

3

4

5

6

7

8

9

10

11

12

13

E-Paper

Newspaper

BN

Budget 2025-2026

Eid ul Azha Special

Online Version

Print Version

Special Issue

Bangladesh's Cooling Boom - Online Version

Bangladesh's Cooling Boom - Print Version

14th-Anniversary Special Issue-01

14th-Anniversary Special Issue-02

14th-Anniversary Special Issue-03

14th-Anniversary Special Issue-04

Eid Magazine 2024

ICC Champions Trophy 2025

Photo Gallery

Latest

More News

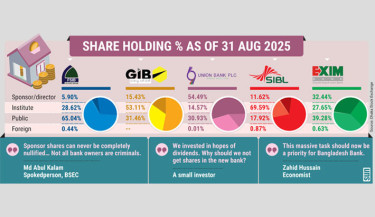

Five-bank merger sparks investor worries

Concrete span, broken hopes: Gaibandha awaits the road ahead

Tax bounty leaves out majority of Indian workforce, missing growth stimulus

A ray of hopes after unrest and tension?

Padma Bridge: Boon exceeds hopes in 2 yrs

Tigers depart for T20 World Cup with small hopes

US investments to Bangladesh will increase more, hopes Kamal

Billion-euro bill for business as France hopes riots over

Trending

Political commitment key to neutral public administration

Attempt to circulate counterfeit notes before polls

Sluggish growth looms for Bangladesh due to geopolitical tensions

More focus required on sending skilled workers abroad

1 killed, 2 injured in BNP’s factional clash in Munshiganj

Fakhrul alleges attempt to erase Liberation War history

New committee formed for Bashundhara Shuvosangho DU unit

Security tightened at religious sites after crude bomb explosions in Dhaka

Educational, cultural festival held in Joypurhat

Tariff Commission proposes increase in soybean oil price

Gazipur students tests their blood groups through free campaign

Bangladesh’s reserves still remain above $31 billion after ACU payment

Moyeen Khan calls for united efforts to build democratic Bangladesh

Tarique calls emergency Standing Committee meeting Monday night

US senators reach deal that could end record shutdown

Admission application from 21 Nov, selection through lottery

China rolls out its version of the H-1B visa to attract foreign tech workers

Govt may compensate investors in 5-bank merger: BB

Bus set on fire near Labaid Hospital in Dhanmondi

NCP ready for both ‘ballot and bullet’ revolution: Nasiruddin Patwary

Shanto backs Salahuddin amid resignation talks

Italy eyes stronger ties, lawful migration with Bangladesh

NBR launches online VAT refund module

Denmark launches new partnership to strengthen rights, mental health, media freedom in Bangladesh

BIMSTEC secretary general meets ADB president, others

Trump threatens legal action against BBC

UAE 'probably' won't join Gaza stabilisation force: Senior Official

EC to invite 56 political parties in nine groups to dialogue

Bangladesh’s overheated onion market costs consumers Tk3.5cr more every day

Don’t test patience of July revolutionaries: Press Secy to AL supporters