Saturday 15 November 2025

Latest

E-Paper

বাংলা

Previous Month

November 2025

January

February

March

April

May

June

July

August

September

October

November

December

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Su

Mo

Tu

We

Th

Fr

Sa

26

27

28

29

30

31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

1

2

3

4

5

6

7

8

9

10

11

12

13

E-Paper

Newspaper

BN

Budget 2025-2026

Eid ul Azha Special

Online Version

Print Version

Special Issue

Bangladesh's Cooling Boom - Online Version

Bangladesh's Cooling Boom - Print Version

14th-Anniversary Special Issue-01

14th-Anniversary Special Issue-02

14th-Anniversary Special Issue-03

14th-Anniversary Special Issue-04

Eid Magazine 2024

ICC Champions Trophy 2025

Photo Gallery

Latest

More News

EU ambassador calls for policy stability in Bangladesh after election

BB formulating AI policy to boost security, efficiency in banking

National Logistics Policy 2025 approved to boost investment, exports

Extreme poverty hinders economic growth

Former American strategy of ‘regime change’ is over: Tulsi Gabbard

New Pentagon policy undercuts trans troops' ability to ask to stay in the military

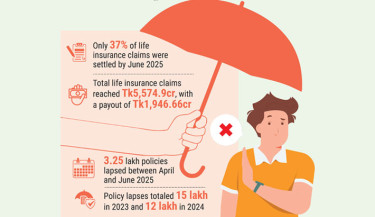

Insurance sector reels from policy lapse wave

Washington Post, New York Times, AP, Reuters, Atlantic and more outlets reject Pentagon policy

Trending

Chief justice expresses deep concern over killing of Rajshahi judge’s son

AI Integration into Tertiary Education: Opportunities and Challenges

Bangladesh to open embassies in Dublin and Buenos Aires

People’s aspirations ignored by calling two votes on same day: Parwar

Ali Riaz appointed special assistant to CA

Referendum: One question, four issues on ballot

Japan PM Takaichi says she sleeps only 2-4 hours a night

Discussion on role of youth leadership in social change held at RU

Taijul becomes third Bangladeshi bowler to claim 500 First-Class wickets

Hamza heroics in vain as late goal denies Bangladesh win against Nepal

DU VC nominated as Bangladesh’s next ambassador to Denmark

Gold price rises to Tk2.13 lakh per bhori

EU urges parties to engage in next steps of democratic transition

Friendly football match held to discourage drug abuse

Blood groups of 200 students detected in Abhaynagar, Jashore

15 underprivileged women receive sewing machines in Monpura

BNP thanks CA for announcement of holding polls, referendum on same day

JASAS organises cultural event marking National Solidarity Day

BNP inaugurates month-long video competition centred on ex-president Ziaur Rahman

Pakistan’s president assents 27th Amendment to law

PBI to probe attempted murder case against actor Dipjol

Judge’s son stabbed to death at house in Rajshahi city

EC to respond to referendum after getting formal request from govt: CEC

Man sentenced to death for killing girlfriend in Kalabagan

Editors’ Council gets new body

Hamza, Zayan injuries not serious ahead of India clash

No one knows why Bangladesh broke down late, not even the coach

Dismembered body found inside two drums near Nat'l Eidgah

Abdus Salam appointed MD of Dhaka WASA

Rubio dismisses criticism of US Caribbean strikes