Saturday 08 November 2025

Latest

E-Paper

বাংলা

Previous Month

November 2025

January

February

March

April

May

June

July

August

September

October

November

December

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Su

Mo

Tu

We

Th

Fr

Sa

26

27

28

29

30

31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

1

2

3

4

5

6

7

8

9

10

11

12

13

E-Paper

Newspaper

BN

Budget 2025-2026

Eid ul Azha Special

Online Version

Print Version

Special Issue

Bangladesh's Cooling Boom - Online Version

Bangladesh's Cooling Boom - Print Version

14th-Anniversary Special Issue-01

14th-Anniversary Special Issue-02

14th-Anniversary Special Issue-03

14th-Anniversary Special Issue-04

Eid Magazine 2024

ICC Champions Trophy 2025

Photo Gallery

Latest

More News

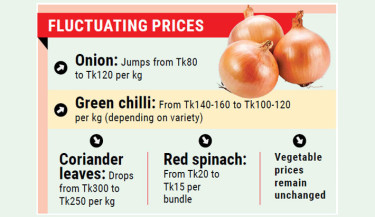

Onion price soars, vegetable market remains stable

Bangladesh writes to Malaysia seeking relaxation of three conditions

Illegal phones dominate 60% of market, industry warns

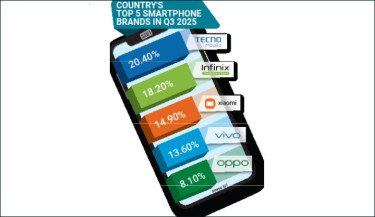

Value for money redefines Bangladesh’s smartphone market

Shwapno’s Rise: From struggling outlets to Bangladesh’s most popular retail giant

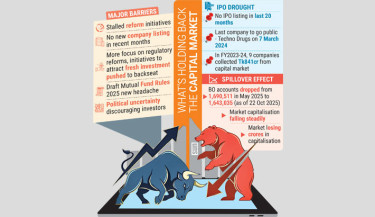

Capital market reform initiatives fall flat

Tk2,500cr govt bond to fund development in 3 southeast dists

Malaysia labour market may again fall into syndicate control

Trending

Dustbins donated to madrasa in Dinajpur

Rajnath reiterates India’s unwillingness to have tense relations with Bangladesh

BNP suspends three Sitakunda leaders

Sewing training centre launched at school in Moulvibazar

Campaign calls for avoiding online gambling in Gaibandha Sadar

Those opposing referendum are afraid of DUCSU elections: Taher

BCB divided over suspected cricketers’ participation in BPL

NCP holds celebratory rally in Mirpur after gaining registration, ‘Shapla Kali’ symbol

Nation rallies behind Jahanara

Bashundhara Strikes defeat Grameenphone for its third win in a row

Three champions emerge as Bashundhara Kings Academy Future legends Tournament concludes

Defetishising World University Rankings and Debunking Neoliberal Myths

BNP stages major rally ahead of polls

Shakib Khan appears with new look of ‘Soldier’

Alibaba Ebong Chollis Chor premieres at Shilpakala today

‘Going beyond consensus will deepen division’

Earth can no longer sustain intensive fossil fuel use: Lula

‘Toggi Toys’ opens new outlet at Bashundhara City Shopping Mall

SOLO EXHIBITION ‘VISIBLE–INVISIBLE’ KICKS OFF IN THE CITY

31 held in Dhaka ahead of AL’s 13 Nov lockdown

BNP bets on veterans as Jamaat introduces fresh candidates in Cox’s Bazar

China Is Set to Lead the New World

Price of Corruption in a Warming World

Brazil welcomes China lift of ban on poultry imports

Living under Terrorism: The CHT’s Criminal Empires

Govt ultimatum ends tomorrow amid deadlock over referendum timing

A candidate requires Tk10-20 crore to contest elections: Adviser Asif Mahmud

Shammo killed for opposing cannabis sale at Suhrawardy Udyan

3 policemen among 25 injured as BNP factions clash in Faridpur

Raw materials used to produce heroin entering Bangladesh from Myanmar