Friday 14 November 2025

Latest

E-Paper

বাংলা

Previous Month

November 2025

January

February

March

April

May

June

July

August

September

October

November

December

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Su

Mo

Tu

We

Th

Fr

Sa

26

27

28

29

30

31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

1

2

3

4

5

6

7

8

9

10

11

12

13

E-Paper

Newspaper

BN

Budget 2025-2026

Eid ul Azha Special

Online Version

Print Version

Special Issue

Bangladesh's Cooling Boom - Online Version

Bangladesh's Cooling Boom - Print Version

14th-Anniversary Special Issue-01

14th-Anniversary Special Issue-02

14th-Anniversary Special Issue-03

14th-Anniversary Special Issue-04

Eid Magazine 2024

ICC Champions Trophy 2025

Photo Gallery

Latest

More News

Shanto on sabbatical: “focused on enhancing my cricket”

Shanto hails Murad’s debut, Joy’s comeback in Bangladesh Win

Shanto lauds team effort as Bangladesh dominate Ireland

Bangladesh crush Ireland by an innings to sweep Sylhet Test

Lack of control over hybrid seed prices burdens Sunamganj farmers

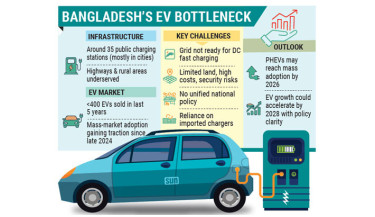

EV sector rises, charging network lags behind

No one knows why Bangladesh broke down late, not even the coach

Hamza, Zayan injuries not serious ahead of India clash

Trending

Chief justice expresses deep concern over killing of Rajshahi judge’s son

Bangladesh to open embassies in Dublin and Buenos Aires

Hamza heroics in vain as late goal denies Bangladesh win against Nepal

EU urges parties to engage in next steps of democratic transition

Blood groups of 200 students detected in Abhaynagar, Jashore

Gold price rises to Tk2.13 lakh per bhori

BNP thanks CA for announcement of holding polls, referendum on same day

JASAS organises cultural event marking National Solidarity Day

15 underprivileged women receive sewing machines in Monpura

Pakistan’s president assents 27th Amendment to law

EC to respond to referendum after getting formal request from govt: CEC

Hamza, Zayan injuries not serious ahead of India clash

No one knows why Bangladesh broke down late, not even the coach

Abdus Salam appointed MD of Dhaka WASA

Rubio dismisses criticism of US Caribbean strikes

‘Ukraine must negotiate with Russia sooner or later’

Nine more districts get new DCs

Fakhrul sees Feb polls as a chance for truly representative parliament

Bangladesh take silver after final defeat in Table Tennis

PKSF Day celebrated marking 35th anniversary

EV sector rises, charging network lags behind

Unity is victory, division is decay

BNP candidate stages daylong sit-in on Dhaka-Chattogram highway

Top officials hired with invalid experience certificates

Be ready for 21st-century challenges, Army Chief tells Bangladesh Infantry Regiment

Referendum, nat’l polls on same day: CA

Dhaka Senior Division Football League back with 18 teams

Riyadh’s Al-Suwaidi Park turns into mini Bangladesh

Shanto’s evolving blueprint

Development budget cut by Tk30,000 crore