Wednesday 05 November 2025

Latest

E-Paper

বাংলা

Previous Month

November 2025

January

February

March

April

May

June

July

August

September

October

November

December

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Su

Mo

Tu

We

Th

Fr

Sa

26

27

28

29

30

31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

1

2

3

4

5

6

7

8

9

10

11

12

13

E-Paper

Newspaper

BN

Budget 2025-2026

Eid ul Azha Special

Online Version

Print Version

Special Issue

Bangladesh's Cooling Boom - Online Version

Bangladesh's Cooling Boom - Print Version

14th-Anniversary Special Issue-01

14th-Anniversary Special Issue-02

14th-Anniversary Special Issue-03

14th-Anniversary Special Issue-04

Eid Magazine 2024

ICC Champions Trophy 2025

Photo Gallery

Latest

More News

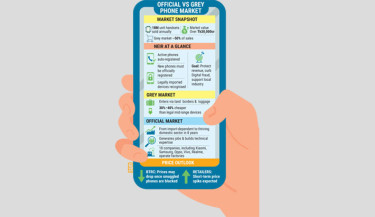

Digital crackdown: Can NEIR defeat the grey phone empire?

Nasim named digital media icon

Seminar on ‘Digital Contents: Information, Risk and Ethics’ held at JU

Jahidul Islam honoured with Digital Media Excellence Award

Initiative to bring youths back to sports to curb digital device addiction

Digital tracking to ensure transparency in Ansar’s election duties: DG

Akij Resource unveils plan for Shariah-based digital bank

Capital shortfall rises to Tk1.55 lakh crore in 24 banks

Trending

NCP yet to announce its official list of candidates: Tusher

Nayab Yusuf secures BNP nomination for Faridpur-3 constituency

Nusraat Faria joins Tania Brishty, Moushumi Hamid in new film!

Exports fall 7.43% in October 2025

BNP announces 13 candidates for Dhaka’s constituencies

Ashraful to join national team as batting coach, Razzak named team director

BCB introduces new clause to penalise boycotting clubs

bKash, Robi, Banglalink and other conglomerates line up for digital bank licence

Bangladesh’s Economic Struggle Continues

CA’s visionary decision and the responsibility of political parties

Turkish parliamentary delegation meets CA

Netherlands launches visa centre in Dhaka

BNP names candidates for 237 seats, 63 open for allies

Sohan, Shoriful racing against time to be fit for Ireland series

BNP faction blocks Dhaka-Ctg highway as Aslam excluded from draft candidate list

ACC sues Salman, 32 others for looting Tk1,950cr from Janata Bank

National Elections: BNP names 10 women candidates in draft list

Empathy: A Leadership Skill We Cannot Afford to Ignore

Obstacles to Making Our Bureaucracy Functional

Sri Lanka U-17 set for Bangladesh tour

Bangladesh moves to boost smartphone access for marginalised communities

Brahmanbaria-2: BNP keeps Rumeen Farhana’s seat in limbo

Thousands flee as Sudan conflict spreads east from Darfur: UN

‘Heroic’ worker praised as man charged over UK train stabbings

Denmark inaugurates rare low-carbon hydrogen plant

Forest officer injured in poacher attack in Sundarban; 3 detained

Candidates must contest under own party symbol even in alliances

Old syndicate looms over Malaysia’s labour recruitment from Bangladesh

Crisis intensifies in garment sector

Jamaat to announce final candidates soon: Shafiqur Rahman