Tuesday 11 November 2025

Latest

E-Paper

বাংলা

Previous Month

November 2025

January

February

March

April

May

June

July

August

September

October

November

December

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Su

Mo

Tu

We

Th

Fr

Sa

26

27

28

29

30

31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

1

2

3

4

5

6

7

8

9

10

11

12

13

E-Paper

Newspaper

BN

Budget 2025-2026

Eid ul Azha Special

Online Version

Print Version

Special Issue

Bangladesh's Cooling Boom - Online Version

Bangladesh's Cooling Boom - Print Version

14th-Anniversary Special Issue-01

14th-Anniversary Special Issue-02

14th-Anniversary Special Issue-03

14th-Anniversary Special Issue-04

Eid Magazine 2024

ICC Champions Trophy 2025

Photo Gallery

Latest

More News

Nine Kuwaiti planes make emergency landings in Iraq due to dense fog

Death toll from UPS plane crash in Louisville rises to 14

Fire at Rooppur Nuclear Power Plant under control

Seven trapped after S Korea power plant structure collapse

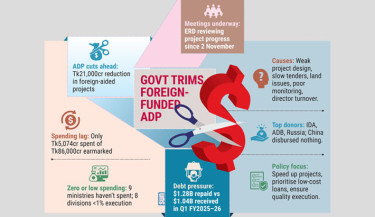

Foreign-aided projects falter, Tk21,000cr cut in revised ADP

Denmark inaugurates rare low-carbon hydrogen plant

Turkey to hold Gaza peace plan meeting for Muslim states

$1 on family planning to save Bangladesh $14: UNFPA

Trending

Germany to fund data, research centre in Dhaka

BNP to create human resources to build a new Bangladesh: Khasru

Gold price rises to Tk2.04 lakh per bhori

Those who dream of changing Bangladesh must step into politics: Nahid

EC to invite 56 political parties in nine groups to dialogue

Bus set on fire near Labaid Hospital in Dhanmondi

13 killed in blast near Delhi Red Fort

Land, apartment fraud

Politics heats up over referendum

Multiple explosions, arson attacks reported in Dhaka

DMP restricts mobile phone use for on-duty police to boost vigilance

Bangladesh High Commissioner in Delhi mourns deaths in Red Fort blast

On Law against Enforced Disappearances

Trump threatens legal action against BBC

Why scrapping of music teacher post in pry schools not illegal: HC

Primary teachers withdraw movement as govt promises 11th grade benefits

Navy rescues 24 fishermen from Bay of Bengal

99 and counting: Mushfiqur Rahim nears Test history

Bangladesh’s endless battle with river erosion

Shanto’s Sylhet Déjà Vu: Bangladesh above self, faith renewed in BCB

Production or demand — where’s the miscalculation?

What happened, who voted to end it, what’s next?

France's Sarkozy back home after court frees him pending appeal

Only the chief adviser can untie this knot

Bullseye on the field, blindfolded on safety

Tigers return to Test cricket eyeing big scores and milestones

ACC files case against CRI over tax evasion, money laundering

Eight parties set to stage mass rally over 5-point demand

Injured Courtois set to miss Belgium World Cup qualifiers

Crude bomb, arson attacks trigger tightened security across Dhaka