Thursday 06 November 2025

Latest

E-Paper

বাংলা

Previous Month

November 2025

January

February

March

April

May

June

July

August

September

October

November

December

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Su

Mo

Tu

We

Th

Fr

Sa

26

27

28

29

30

31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

1

2

3

4

5

6

7

8

9

10

11

12

13

E-Paper

Newspaper

BN

Budget 2025-2026

Eid ul Azha Special

Online Version

Print Version

Special Issue

Bangladesh's Cooling Boom - Online Version

Bangladesh's Cooling Boom - Print Version

14th-Anniversary Special Issue-01

14th-Anniversary Special Issue-02

14th-Anniversary Special Issue-03

14th-Anniversary Special Issue-04

Eid Magazine 2024

ICC Champions Trophy 2025

Photo Gallery

Latest

More News

Extreme poverty hinders economic growth

Political crisis began with caretaker government verdict: BNP tells Appellate Division

Global water crisis could cost trillions

Bangladesh Must Learn to Earn from the Green Climate Fund

Business slump deepens revenue shortfall

Gaza health crisis will last for generations

Middleclass Are Worst Hit in Economic Turmoil

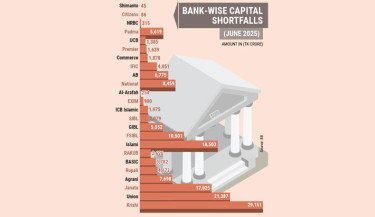

24 banks in capital crisis amid widening corruption scandal

Trending

Army wants free and fair election: Lt Gen Mainur

Who Will Bell the Cat?

Bangladesh above all

Hidden and open scheming over the port

Administration now under the grip of bureaucrats appointed on contract

Hyder Husyn on Music as Soulwork

Five banks’ share trading put on hold

Politics: Old Wine in New Bottle

Trump and Xi Jinping – Who Deserves the Smile!

Effective Internal Audit:The Cornerstone of Bank & FI

What Mamdani’s win means for the Big Apple and beyond

Referendum must be held before national election: Jamaat’s Taher

Federal judge in Chicago orders clean toilets, access to lawyers for immigration detainees

Value for money redefines Bangladesh’s smartphone market

Reza Kibria joins BNP, intends to contest from Habiganj-1

Tarique Rahman urges nationalist forces to unite for stronger democracy

Jamaat warns of tough movement in capital if demands remain unmet on 11 Nov

Trump says lost 'sovereignty' in New York after Mamdani win

Police intercept Jamaat, Islami Andolon procession near Matsya Bhaban

Over 80,000 non-immigrant visas revoked under Trump administration

5-year jail, Tk99cr fine for spreading communal hatred online

'Hostage diplomacy': longstanding Iran tactic presenting dilemma for West

Govt approves holiday list for next year

BNP keeps 64 seats open for allies amid electoral symbol challenge

Former BB deputy governor SK Sur indicted in graft case

Islamic parties march towards Jamuna demanding referendum in Nov

US orders 10% flights cut at major US airports due to shutdown

EC plans to use schools, colleges CCTV cameras for national polls

Announce election schedule without delay: Fakhrul

Govt approves ordinance with death penalty for enforced disappearance