Tuesday 16 September 2025

Latest

E-Paper

বাংলা

Previous Month

September 2025

January

February

March

April

May

June

July

August

September

October

November

December

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Su

Mo

Tu

We

Th

Fr

Sa

31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

1

2

3

4

5

6

7

8

9

10

11

E-Paper

Newspaper

BN

Budget 2025-2026

Eid ul Azha Special

Online Version

Print Version

Special Issue

Bangladesh's Cooling Boom - Online Version

Bangladesh's Cooling Boom - Print Version

14th-Anniversary Special Issue-01

14th-Anniversary Special Issue-02

14th-Anniversary Special Issue-03

14th-Anniversary Special Issue-04

Eid Magazine 2024

ICC Champions Trophy 2025

Photo Gallery

Latest

More News

Sonali Life Insurance wins Commonwealth Business Excellence Awards 2025

Top five companies dominate insurance sector

Some thoughts on developing non-life insurance sector

Some thoughts on developing non-life insurance sector

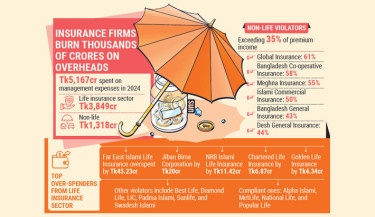

Many insurers breach spending limits, IDRA flags risk

CEO shortage sparks mismanagement, erodes trust in insurance sector

Insurance cos often unwilling to provide accurate info: IDRA chairman

BMMDP introduces two transformative initiatives

Trending

Sri Lanka cruise to six-wicket win over Bangladesh

Trade conference held in China with participation of Bangladeshi business representatives

Last-gasp Juve beat Inter to maintain perfect Serie A start

Chelsea blow chance to top Premier League at Brentford

Atletico beat Villarreal for first Liga win

Newly-elected JUCSU VP Zitu vows end of partisan politics on campus

Chief Adviser mourns death of noted folk singer Farida Parveen

Govt condemns attempted attack on Mahfuj Alam in London

Killing Hamas leaders is route to ending Gaza war: Netanayhu

Impact of Potato Price Fixing

Reject cruelty, embrace humanity: Tarique Rahman

Democracy is not a paper document – it’s a practice

After DUCSU and JUCSU, Student Politics Facing a Dilemma

Skyrocketing prices of baby food

DUCSU’s first meeting starts

CUCSU polls nomination paper distribution starts

Crunch talks on July Charter as deadline expires tomorrow

Suspected gang attack in Ecuador kills seven

Post-mortem of Parallels and Contrasts: Nepal, Sri Lanka and Bangladesh

Four firms approved to make govt-standard battery rickshaws

US trade team will reach Dhaka today to discuss further reduction in tariffs

Drizzles in Dhaka: A rough start to week for commuters

Secret Strategies Will Plunge the Nation into Crisis

Disagreements over post-sharing stalls anti-Shibir bloc formation talks at CU

Khulna BSCIC fails to emerge as viable industrial hub

Trade conference in China: Active participation of Bangladeshi businessmen

Urban Youth climate Conference 2025 held in Dhaka

Lab-grown diamonds robbing southern Africa of riches

Sadhan Chandra turned Food Ministry into corruption hub

Hotels, restaurants evade Tk18,000cr in VAT annually