Friday 14 November 2025

Latest

E-Paper

বাংলা

Previous Month

November 2025

January

February

March

April

May

June

July

August

September

October

November

December

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Su

Mo

Tu

We

Th

Fr

Sa

26

27

28

29

30

31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

1

2

3

4

5

6

7

8

9

10

11

12

13

E-Paper

Newspaper

BN

Budget 2025-2026

Eid ul Azha Special

Online Version

Print Version

Special Issue

Bangladesh's Cooling Boom - Online Version

Bangladesh's Cooling Boom - Print Version

14th-Anniversary Special Issue-01

14th-Anniversary Special Issue-02

14th-Anniversary Special Issue-03

14th-Anniversary Special Issue-04

Eid Magazine 2024

ICC Champions Trophy 2025

Photo Gallery

Latest

More News

Govt issues Tanguar and Hakaluki Haors Protection Order

Stronger NGO–govt cooperation urgent for better services, speakers say

Workshop on mental health protection organised in Faridpur

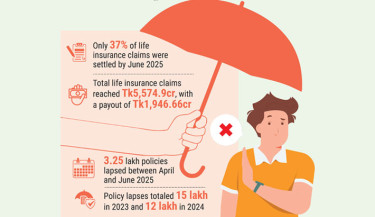

Insurance sector reels from policy lapse wave

Weak insurers next in merger plan

Insurance claims may take weeks to process

CPJ demands Myanmar rebels immediately release female journalist

How a Term Insurance Plan Can Protect Your Family

Trending

EV sector rises, charging network lags behind

BNP candidate stages daylong sit-in on Dhaka-Chattogram highway

Unity is victory, division is decay

Be ready for 21st-century challenges, Army Chief tells Bangladesh Infantry Regiment

Development budget cut by Tk30,000 crore

Riyadh’s Al-Suwaidi Park turns into mini Bangladesh

Referendum, nat’l polls on same day: CA

One vote on 4 points could confuse voters, warn experts

I never issued any order to fire on unarmed civilians, Hasina tells BBC

Top officials hired with invalid experience certificates

Polls to be inclusive; AL won't be able to take part: CA Yunus

UK minister calls on Chief Adviser

‘Religious opportunists’ want to keep women indoors: Salahuddin

Trump sprays Syria’s Al-Sharaa with perfume, asks how many wives he has

Chief Adviser’s recent speech shows clear favouritism towards a single party: Taher

Bangladesh seeks urgent adaptation finance at COP30

Apple and OpenAI must face X Corp's lawsuit for now, US judge rules

Sewing training centre opens for underprivileged trainees in Moulvibazar

‘Ishara’ receives warm reception from audience

US pressures UN Council to adopt Trump’s Gaza peace plan

Lack of control over hybrid seed prices burdens Sunamganj farmers

Hasina’s fate to be sealed on 17 Nov

Osman Hadi receives death threats from 30 numbers

Health diplomacy: New Rx for China-Bangladesh friendship

Sramik Dal leader shot dead in Rangunia

‘JnUCSU Photo Contest’ kicks off 16 November

‘Audience will always be there only if the story is solid’

Bangladesh crush Ireland by an innings to sweep Sylhet Test

Nagad urges customers not to worry about Google Play Protect warning on app

Teen drowns in Turag River while fleeing after setting bus on fire