Friday 26 April 2024

E-Paper

বাংলা

Previous Month

April 2024

January

February

March

April

May

June

July

August

September

October

November

December

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

Su

Mo

Tu

We

Th

Fr

Sa

31

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

1

2

3

4

5

6

7

8

9

10

11

E-Paper

Newspaper

BN

Eid Magazine 2024

Photo Gallery

More News

IFC to lend $30m to Pran-RFL for easing dollar crunch

Tk30 crore borrowed from banks with false NIDs

Bank lending rate tops 13.55% in April

Photography exhibition ‘Bangladesh in Frames’ going on in Mexico’s Queretaro

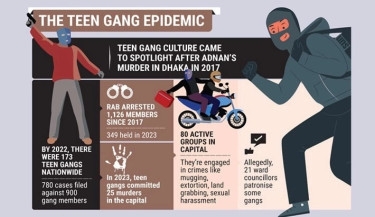

Teen Gang Culture: A Call for Comprehensive Action

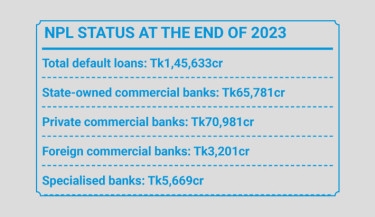

Default loans surge 21% in 2023

Culture Shock Experienced by International Students in the US

Loan disbursement in sustainable finance sector drops

Trending

India keeps a close watch on China–Bangladesh joint military exercise

Ukraine access to US long-range missiles will not impact war: Russia

Macron warns Europe could ‘die,’ needs stronger defence

Preeti Urang’s death: Efforts to hide crime feared

Body count nears 400 in Gaza hospital mass graves

Pro-Palestinian US university protests grow as police crack down

Cargo vessel capsizes in Bay of Bengal with12 crew

CUET VC confined as students refuse to vacate halls

100% Waiver on Admission Fees at the Canadian University of Bangladesh

Cuet students set fire to bus protesting closure

Collaboration between Bangladesh and KSA in Higher Education, Training and Research

DNCC officials binge on Tk3,600/kg biscuits using emergency funds

Schools, colleges to reopen Sunday

Fire in hospitals, clinics on the rise

Bangladesh: The Untapped Powerhouse of Global Halal Market

Paoli Dam stars in Bangladeshi film again

PM seeks Thai investment in Bangladesh medical facilities

Dhaka’s air quality ‘unhealthy’ this morning

Mass awareness imperative for preventing heat-related illness

PM Hasina opens bilateral meeting with Thai premier Thavisin

Coach said it would be fine if I play two matches: Shakib

Indian election resumes as heatwave hits voters

Cluster admission test for 24 public varsities from 27 Apr

IPL success makes cricket easier for Mustafizur

Amitabh Bachchan receives Lata Mangeshkar Award

New drama serial ‘Roser Hari Barabari’

A class should not exceed 55 students

Rain likely to drench Ctg and Sylhet divisions

Hypocrisy: a disease of the heart

Bangladesh, Thailand have scopes to boost cooperation in different fields: PM